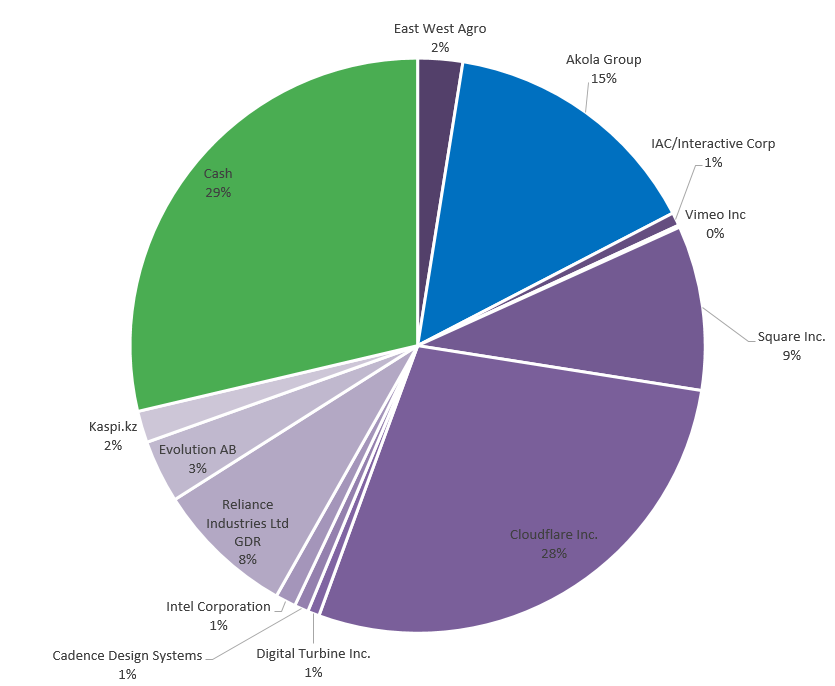

Increased AKO1L (Akola Group) position by 40% ahead of FY 2024-2025 earnings. Too bad I was busy to absorb stellar Q2-Q3 reports in time, price ran away quite a bit.

Few comments why:

-Q2, Q3 profit drivers were poultry and raw milk. Chicken pox in Poland, supply constraints after market downturn forced some players out, and prices, that kept rising throughout Q4 (end June 30)

-wholesale electricity prices were more muted in Q4, with highly windy June In Baltics

-Alytus factory in Q3 was still undergoing machinery calibration with revenue ramping under pressure and added cost, both of which should be gone by Q4 (according to CFO)

-although raw milk prices are on decline, they are still +30% YoY for July in Lithuania

-revised EBITDA guidance for FY from 70-90 -> 80-100M EUR

Too much hastle nowadays to attach pics on nostr, besides I don't even know if note is saved on any relay anyway.

ref:

X (formerly Twitter)

Generalist Lab (@Generalist_Lab) on X

1/3

Increased AKO1L (Akola Group) position by 40% ahead of FY 2024-2025 earnings. Too bad I was busy to absorb stellar Q2-Q3 reports in time, price...